Since COVID-19 hit the world in an unexpected way, it has demonstrated to corporates that the easily neglected ‘non-financial’ factors are indeed equally important to long-term sustainability of businesses. The concern on ESG issues is higher than ever before

ESG reporting in the Asia Pacific

While the EU has always been a pioneer in ESG reporting, the Asia Pacific region is now catching up in building a more sustainable economy. Asia Pacific countries such as Hong Kong, Australia, Japan, Singapore, Thailand, Taiwan, etc. have already established disclosure and reporting requirements and guidelines.

In 2019, HKEX took a step ahead toward sustainability by introducing new amendments to tighten ESG regulatory framework, including making at least part of the ESG reporting mandatory for listed companies. This puts Hong Kong in a leading position regarding ESG regulatory and policy governance and disclosure.

The amendments include a number of significant changes to the regulatory framework for ESG disclosures but most importantly, HKEX amendments aim to put ESG on the board. The idea is to make the boards play a leadership role and be accountable for ESG reporting, imposing a fiduciary duty on the board to engage in developing strategies with respect to ESG, and to get involved in the entire process from oversight to reporting. This can help drive companies to focus more on meeting the treble bottom lines.

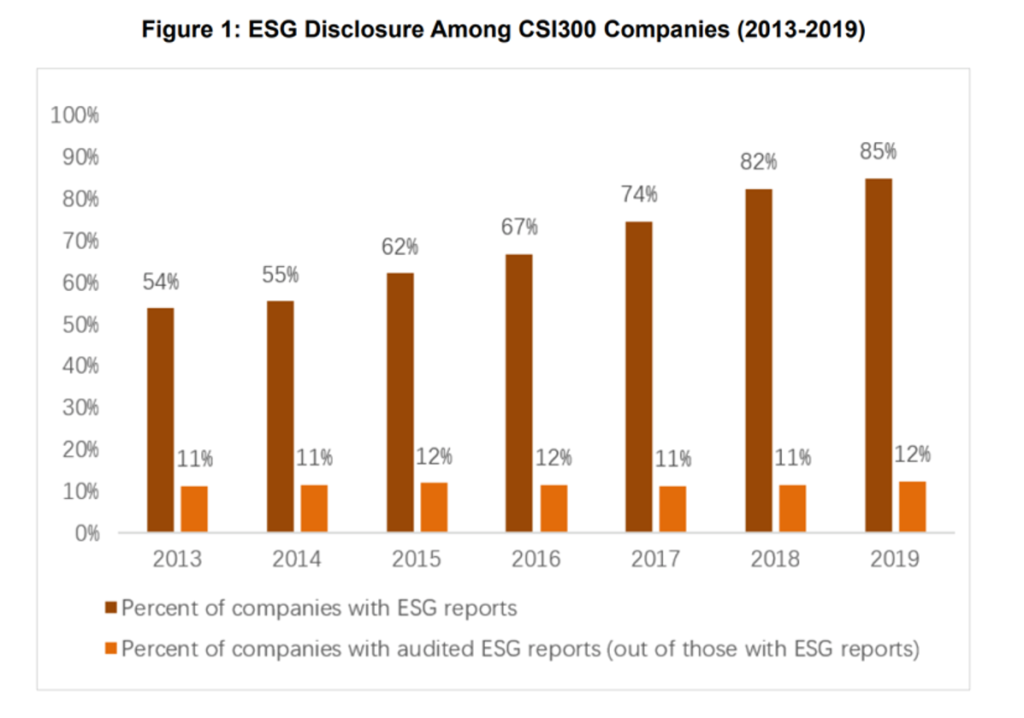

China is also taking steps to achieve sustainability. According to the graph below, it can be seen that there has been a steady increase in the percentage of companies with ESG reports.

Source: Analysis of Wind data

China’s goal to achieve carbon neutrality by 2060 constitutes a move to put a sharper focus on transitioning into a low-carbon economy. In order to catch up with global developments, in 2020, China Securities Regulatory Commission also formulated plans to enforce regulations requiring listed companies to disclose environmental information.

Hong Kong’s continuous efforts in sustainability reporting

Prior to the new amendments, Hong Kong has been putting in efforts to transition itself into a more sustainable global financial hub. Hong Kong has been an active partnership with Sustainable Stock Exchanges Initiative since 2018. With recent HKEX amendments, Hong Kong is moving upwards in the rankings for sustainability. Moreover, the new requirements are setting new global trends of reporting. The introduction of reporting principles of “materiality” is in line with the principle of reporting climate-related information in EU Non-financial Reporting Directive (NFRD). Also, EU and the UK have long ago adopted the principle of ‘comply and explain’, and HKEX by the latest amendments is upgrading the disclosure obligation to cover all Social KPIs.

Apart from that, Hong Kong’s financial sector has also been working towards green finance and incorporating ESG into the industry best practices to keep up with global financial market trends. MPFA issued a circular back in 2018 encouraging application of ESG standards into investments and disclosure. The following year, HKMA incorporated ESG factors in its responsible investment measures while Securities and Futures Commission carried out a survey on ESG integration.

Global cooperation to address challenges

Although ESG reporting is becoming mainstream, we are still at an early stage of the whole sustainability reporting movement. ESG reporting not only focuses on compliance, but also quality that most investors and the public are looking for. For example, according to GRI principles, the quality of data needs to meet a certain standard and have comparability, accuracy, clarity, reliability and timeliness. The complexity of ESG reporting imposes a lot of challenges in terms of effective sustainability disclosure.

In the absence of unified reporting standards, there is a lack of structured base references for companies and investors to benchmark at the global level. Currently, there are varying international reporting standards. Different companies are using different standards in their reporting and the haphazard mix of international frameworks and standards hinders data consistency. Moreover, since there are no global ESG disclosure obligations, we lack a systematic global platform for making ESG data readily available to the public and the investors. The inadequacy of ESG data hinders transparency, reliability, clarity and comparability, making it difficult for companies and investors to compare, analyze and interpret data.

Recognizing this problem, towards the end of 2020, five sustainability standard-setting global organizations, namely CDP, CDSB, GRI, IIRC and SASB announced a shared vision on comprehensive corporate reporting, aiming to provide a globally accepted framework with a coherent standard for providing information to the public in an effective manner. These organisations are collaborating among themselves to slowly take steps for unification of standards. The collaboration between GRI and SASB aims to provide clarity and compatibility, while the collaboration between IFRS and GRI intends to build connectivity between financial and sustainability reporting.

In a post-COVID world, one can expect to see economies and corporates shifting towards prioritizing sustainability and incorporating ESG in their operations. Although more organizations are now promoting ESG and more ESG-conscious investors are emerging, they are still not enough to drive a strong change in the sustainability reporting ecosystem. Global cooperation is required to bring in a unified, systematic and coherent reporting system on an international platform, while regulations from governments are needed to impose mandatory responsibilities and pressure companies. ESG reporting still has a long way to go. Global big brands are taking the lead in ESG disclosure to influence and raise social awareness, international cooperation and government regulations, and we believe sustainability disclosure will develop into a strong and stable trend all over the world.

{kind=link}